Here’s How Financial Planners Need To Lobby – A Lesson From The Pharmacy Guild

There’s a lot of change happening in the financial planning industry here in Australia. Financial Planners are dealing with the Royal Commission recommendations, FASEA changes including the financial advisor exam, uncertainty around business models and valuations, increased ASIC scrutiny as well as making sure we keep up with our ongoing service obligations. On top of this, you need to respond to legislative changes that affect your clients. And we haven’t had to deal with a market downturn for a while either.

We need strong lobbying on our behalf. And I’m not sure that’s happening.

Full disclosure – I’m an FPA member and have been a CFP for many years. I know the FPA does a great deal of lobbying and has provided a lot of input into the Royal Commission and FASEA changes. The AFA has also been lobbying. And I appreciate the efforts that both these organisations have been making because, frankly, most planners don’t get involved themselves, but they’re quick to criticise their professional bodies, judging them on their results and not understanding the efforts they’ve been making.

But recent events lead me to conclude that our professional bodies could be more effective in their lobbying.

Firstly, we saw how the mortgage brokers mobilised as soon as the Royal Commission findings were handed down and the recommendation made to get rid of their trail commissions. Their industry body had ads ready, organised an online petition and the members went on to social media to hammer home the point that their industry was under threat. The government soon backed away from this proposal.

Granted, the MFAA had some high-profile help in the form of Greg Medcraft (a former chair of ASIC) and Mark Bouris. Also, it didn’t hurt that they could bash the banks in the process of making their point. This is not something that financial planners can do.

But over the past couple of weeks, I’ve watched an even bigger example of effective lobbying from the Pharmacy Guild that wouldn’t pass the Pub Test and would definitely fail the best interest duty. And it’s fallen completely under the radar of most Australians.

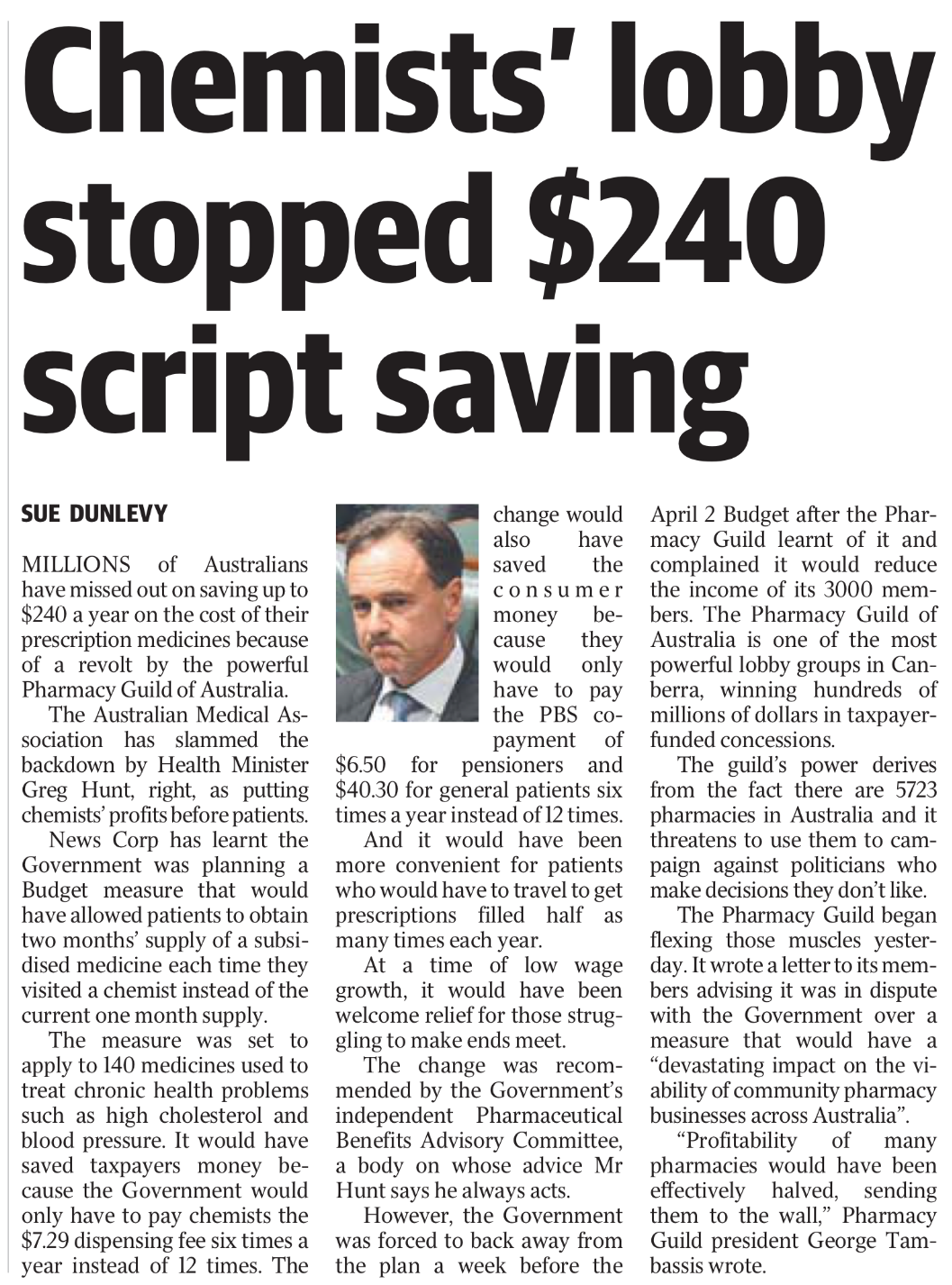

The Adelaide Advertiser ran a story on 29th March titled “Chemists’ lobby stopped $240 script saving”. The article is behind a paywall (here’s a link to an image of the article) but the story goes something like this.

{kind=link}

There are many Australians who are prescribed long-term medication for things like cholesterol and high blood pressure. These are subsidised under the Pharmaceutical Benefits Scheme (PBS) which means that if you’re a Pensioner, you pay a co-payment of only $6.50. If you’re not a pensioner, your co-payment is $40.

Every time a chemist dispenses a script for a PBS drug they receive a $7.29 dispensing fee.

Currently, you can only obtain one packet of medicine at a time. So if you’re on ongoing medicine for your blood pressure, rather than being able to buy two or three month’s worth of your medicine at a time, you have to go to the chemist every month to pick up one packet. And the chemist picks up a $7.29 dispensing fee every month while you pay the co-payment of either $6.50 or $40.

The government had planned a budget measure that would have allowed patients to obtain two month’s supply of their medicine at a time. This would have meant the chemists would only receive one dispensing fee of $7.29 every two months instead of one every month. The article implies that the same would apply to the co-payment amount. A pensioner would only have to pay the $6.50 co-payment every two months under the proposal if they elected to get two month’s supply of their medication. A non-pensioner would only pay their $40 co-payment every second month.

So instead of twelve dispensing payments of $7.29 a year (a total of $87.48), the chemists were only going to receive six payments – a total of $43.74. For the consumer it was even better – imagine only having to pay six co-payments of $40 a year ($240) instead of twelve payments ($480). Saving the consumer $240 a year.

The article says “At a time of low wage growth, it would have been welcome relief for those struggling to make ends meet.”

This proposal seems to make common sense. Especially if you’re someone who is prescribed PBS medicine on an ongoing basis.

But the Pharmacy Guild didn’t think so. They complained that this proposal would reduce the income of its 3000 members.

The article quotes a letter the Pharmacy Guild sent to its members, warning the measure would have a “devastating impact on the viability of community pharmacy businesses across Australia.”

“Profitability of many pharmacies would have been effectively halved, sending them to the wall,” Pharmacy Guild president George Tambassis wrote.

Can we take a moment to reflect on this?

I’m unsure how the profitability of their members would be halved. Last time I checked, my local pharmacy sold a lot more than PBS-subsidised medicines. So whilst receiving less dispensing fees would reduce their income, I think they’ve got enough other products and services to sell that will help their profitability.

Apparently, the Pharmacy Guild is a very powerful lobby group, representing 5723 pharmacies in Australia. With only 3000 members, that implies that some members would own more than one pharmacy. The article says the Guild “is one of the most powerful lobby groups in Canberra, winning hundreds of millions of dollars in taxpayer-funded concessions.”

Wow.

Hundreds of millions of dollars in taxpayer-funded concessions.

Because they are a powerful lobby group. With 3000 members.

I’ve tried to verify the 3000 member number mentioned in the article by visiting the Guild’s website. One of their fact sheets tells me there are 31,212 registered pharmacists in Australia but I couldn’t see anything that showed what their actual membership was. I wonder if membership is aimed at the business level, not at the individual pharmacists.

Either way, it doesn’t matter. This lobby group just managed to stop a government initiative that would have saved taxpayer dollars and made life easier for people who would no longer need to make a monthly trip to a pharmacy.

Here are a couple of ads they ran in our recent Sunday paper, promoting the benefits of the PBS system and suggesting if the Government really wanted to help it could reduce the co-payment. (or maybe the chemists could take a lower dispensing payment?) These ads ran on the front and back pages of the paper – not cheap.

One the one hand, I say well done to them. They clearly have a lot of political clout, and have the ability to influence policy. Did I mention that pharmacists are one of the most trusted professions? Unfortunately, the financial planning profession, especially in a post-Royal Commission world does not enjoy the same levels of trust from the community.

On the other hand, as a tax-payer, I’m dismayed that such a common-sense proposal was removed from the Federal Budget to appease business owners. As someone who has taken a keen interest in the Royal Commission, I’m interested to know how the ‘Pub Test’ and ‘Community Expectations’ could be applied to this decision. I’d love to see Rowena Orr QC examine Health Minister Greg Hunt, and ask him why his government backtracked over a decision that would have saved taxpayers money and made life easier for many Australians.

But that won’t happen. Because … politics. The government needs the Guild members to distribute the PBS-subsidised medication to Australians. Maybe because of this dependency on Guild members the government is less likely to negotiate harder?

The point of this article is not to assess the morality of this decision, but more to ask why the financial planning industry finds it so difficult to put on a united front and have one voice.

The latest ASIC data shows there are over 27,000 financial advisers currently registered. Some of these 27,000 advisers would run their own businesses and employ others. Some would belong to larger institutions that would also employ other people. If we made the assumption that for every adviser there was one other person directly employed by the financial planning industry, you have a figure of over 50,000 people.

50,000 people who vote. And 50,000 people who have long-term relationships with clients who also vote.

This is not an insignificant number.

Yet we have two major professional bodies lobbying government separately. And the AIOFP trying to convince people to become members of the FSU because they have the ear of Labor.

We are far from a unified voice. And we don’t need another industry body. We need to be one voice.

The FPA has over 14,000 members. I’m not sure of the membership of the AFA (it’s not clearly shown on their website). but this article from 2016 has the membership at that point as being over 3,500. As a combined voice, and assuming some membership growth over recent years, these bodies would represent over 18,000 members.

This article has shown you two examples of what happens when industry groups lobby effectively. The MFAA and The Pharmacy Guild have proven that a united voice and a compelling argument can result in good outcomes for members.

Part of the reason our industry is where it is at the moment is that we haven’t had effective lobbying. Yes, our respective industry bodies have lobbied Government, but many would say it has not been done effectively. I wonder what could have happened had our industry bodies come together and lobbied together.

To be clear, I’m not bagging either the FPA or AFA. They’ve done well over a difficult period of time and I can’t help but feel that, to a degree, they’ve been ignored both by the government and the Royal Commission. As industry bodies, they provide a much-needed role and promote the benefits of good financial advice. But their lobbying hasn’t been as effective as many of us would have liked.

And, if it’s not clear by now, I have the belief that more financial advisers should be taking proactive steps to engage with their professional bodies and speak with their local members of parliament about the future of the financial advice industry. Sadly, the advisers I know of who do this are in the minority.

It’s not too late.

I’m not calling for the AFA and FPA to combine and form one super-association. While that would be great and probably in the long term interests of our industry, it’s not practical at the moment.

What I would like to see is the AFA and FPA combining to form one powerful lobby group that represents financial planners with one unified voice. Imagine how much more effective the lobbying and consultation could be if we had one voice instead of the current situation of many voices, all saying slightly different things.

But it’s not just at the association level. I’d love to see every financial planner in this country get in touch with their local member of parliament, meet with them and explain the changes that are occurring in the industry and the impact these changes will have on ordinary Australians who will need to seek financial advice in the future. And remind them that you run a small business and employ people who live in their electorate. And you have clients who also live in their electorate. And let them know the impact of making ill-informed decisions.

And while we’re at it, can we have some tools to engage with the community better and help them understand the relevant issues? This is something the MFAA did well.

But to do this effectively, we need to be clear on what we’re lobbying for.

For many in the industry, the issue of grandfathered trail is over. Most planners accept that by the end of next year, grandfathered trail on investment products will no longer exist. Could the industry have lobbied better on this topic? Possibly. But that horse has bolted. And whilst I’ll acknowledge that some clients will need to remain in grandfathered products, in most cases clients in these products are better off with something else.

In my opinion, the next area for the industry to focus on is insurance commissions. I can see both sides of the arguments on this topic. I understand why a nil-commission environment will lead to lower premiums. But I’m not sure the average Australian wants to pay an upfront fee for insurance. The MFAA led the way with its research around how consumers wanted to pay for mortgage advice and very clearly showed that even though it may be cheaper in the long term, most consumers didn’t want to pay a fee to a mortgage broker.

I understand the potential conflicts of interest that exist around commission, but I also feel that when LIF has played out and insurance commissions are fixed at 60/20, those conflicts of interest are minimised. The potential problem of recommending higher levels of cover than are needed becomes a Best Interest issue and dealt with as part of the Safe Harbour Steps.

Our industry has enough time to make progress on this issue. Do some consumer research to see what the public thinks about paying for insurance. Do your research on whether clients who obtain financial advice end up with more appropriate levels of insurance. Provide evidence of how the right levels of insurance (and advice) makes a difference in the lives of consumers who have been unfortunate enough to claim on their insurance. Obtain evidence from advisers that proves that they also recommend clients reduce levels of cover as their needs decrease (shock, horror!). This shouldn’t happen under a biased commission system yet it does. It speaks volumes about how ethical advisers put their client’s needs first.

We have the ability to make a real impact on the government with our lobbying. But will we?

At this point in time, we don’t need two professional bodies lobbying around many of the same topics on behalf of their members. We need to be like the Pharmacy Guild – a strong, united body that works for its members and puts the fear of God into politicians.

Don’t say it can’t be done. I’ve just shown you how a lobby group representing 3,000 pharmacists convinced the Government to not proceed with a Budget measure that would have saved money.

What more could a lobby group representing over 27,000 financial planners do?

What can you do to make this happen? By all means, contact your professional body and let them know you’d like to see a combined effort. But what personal cost will you incur? Will you make the effort to speak with your local member of parliament? Would you contribute to a fighting fund to lobby more effectively? If 20,000 planners donated $100 each, that would give the industry $2m to fund it’s lobbying activities. That’s a good start. I’m sure the Pharmacy Guild receives good financial support from its members.

I’d love your thoughts and comments. We’re all in this together and I’m always interested in peoples thoughts and perspectives. Leave a comment below and let me know what you think.

0 Comments